Table of Contents

What is an AI bubble?

An AI bubble is a situation where the price of an asset rises far above its real or intrinsic value, driven mostly by speculation, hype, and investor psychology, rather than fundamentals like earnings, productivity, or actual demand.

Every bubble follows a predictable pattern: excitement, overconfidence, and eventually correction.

This article examines whether current AI valuations are supported by fundamentals or whether the gap between capital spending and monetizable demand points toward an emerging AI bubble.

Is AI a bubble?

To become a bubble, AI companies should be valued far beyond their actual revenue, profitability, or realistic growth potential.

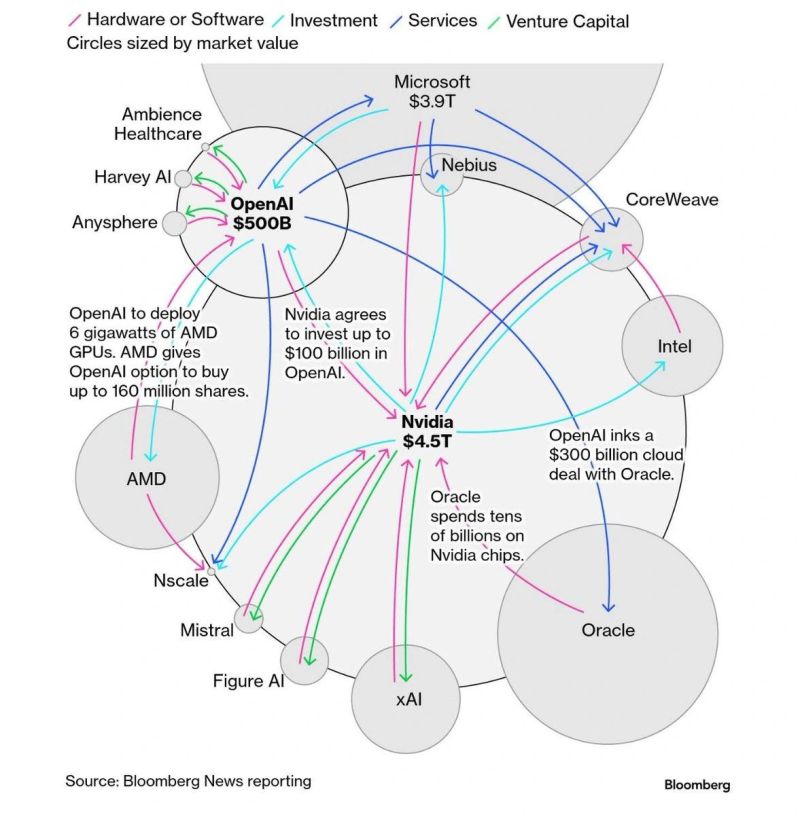

OpenAI, currently the most prominent AI company, is often cited in this debate. Its valuation is estimated at around $500 billion, while reported annual revenue is approximately $14 billion. This implies an exceptionally high valuation multiple, even by technology sector standards.

Nvidia has agreed to invest up to $100 billion in OpenAI. OpenAI utilizes this capital to lease servers from Oracle, on the condition that Oracle purchases its hardware from Nvidia.

Nvidia → OpenAI → Oracle → Nvidia

The concern with round-tripping is not that the transactions are illegal, but that they can distort the appearance of organic demand. When capital circulates among the same parties, reported revenue growth may not reflect true end-user willingness to pay.

This circular investment creates strong financials on paper, but in reality, it is just ‘round-tripping‘. The same capital flows back to the source, meaning no new external income is actually generated.

Round-tripping also occurred during the dot-com bubble. Telecom companies (like Global Crossing, Qwest, and WorldCom) built massive fiber-optic networks. The problem was that they built too much, and not enough people were using them yet. To fake “growth” and revenue, they started swapping capacity with each other. (Source: SEC)

“Currently, the revenues being generated by AI companies and many of the data center operators that are rapidly expanding in order to serve them, are nowhere near big enough to cover their build-out costs. ” – Fortune

OpenAI Debt and Capital Commitments

- $30 billion already borrowed by SoftBank, Oracle, and CoreWeave.

- $28 billion in loans taken by Blue Owl Capital and Crusoe.

- $38 billion on the table in further talks with Oracle and Vantage and their banks.

This totals $96 billion in debt.

OpenAI has secured commitments amounting to $1.4 trillion to acquire the energy resources and computational infrastructure necessary to sustain its future operations. This amount exceeds the GDP of the Netherlands. Such a commitment is extremely ambitious and highlights the scale of capital required to sustain OpenAI’s long-term strategy.

It is important to distinguish between commitments and actual spending. Commitments typically represent long-term agreements that may be conditional, staged, or spread over many years. While they do not imply immediate cash outflows, they still represent binding future obligations that increase financial risk if revenue growth fails to materialize as expected.

In a podcast featuring Sam Altman and Brad Gerstner, Gerstner asked about the $1.4 trillion in commitments, at which point Altman appeared defensive. Altman went on to state that OpenAI would raise capital in part by selling shares of the company.

OpenAI CEO Sam Altman released an internal memo in September 2025 stating that he plans to build up to 250 gigawatts of compute capacity by 2033. This is equivalent to the electricity required to power the entire nation of India and its roughly 1.5 billion citizens. Producing such a large amount of electricity would be extraordinarily difficult and would have significant environmental, logistical, and infrastructure implications.

IBM CEO Arvind Krishna, speaking on the “Decoder” podcast, concluded that there was likely “no way” these companies would earn an adequate return on their massive capital-expenditure spending on data centers.

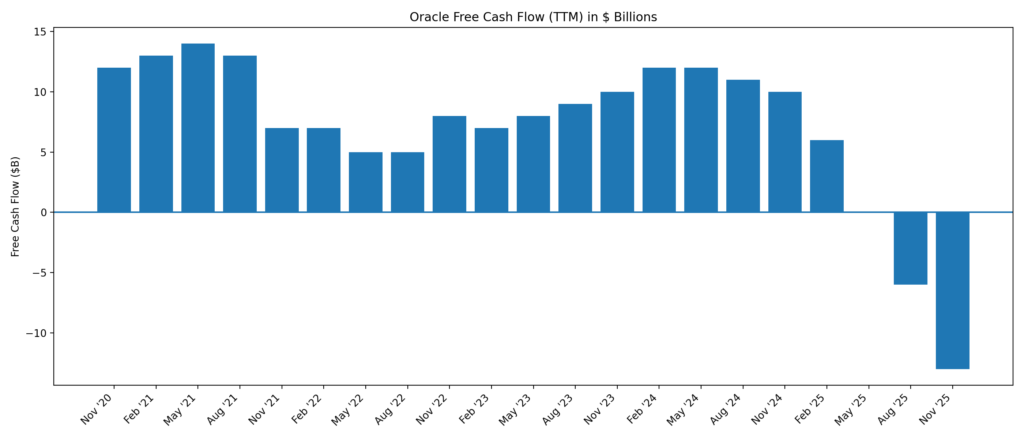

Oracle’s roughly 40% stock decline this fall largely reflects investor concern over its aggressive AI strategy and swelling debt. On one hand, Oracle’s AI partnerships (with OpenAI, SoftBank, Nvidia, etc.) and $523 billion RPO backlog (future revenue commitments) point to a huge growth opportunity. These deals are real and public. On the other hand, funding that growth requires extraordinary spending: Oracle is raising tens of billions in new debt and leases to build out data centers. As one analysis puts it, Oracle’s AI buildout has turned the company from a cash generator into a “free-cash-flow negative” spender, with leverage at multi-year highs.

While Oracle’s RPO backlog signals strong demand visibility, it does not guarantee profitability. Converting backlog into free cash flow depends on execution, pricing power, and the ability to control infrastructure costs as data-center spending accelerates.

While OpenAI is entirely dependent on external revenue and investors, other AI companies can rely on their legacy businesses to help fund GPU purchases and data-center buildouts.

Michael Burry, who famously predicted the 2008 housing crash, has warned that AI may be a bubble and has taken short positions against Nvidia and Palantir. He has deregistered his hedge fund, Scion Asset Management, similar to what he did before the 2008 crash.

On October 31, he tweeted on X: “Sometimes, we see bubbles. Sometimes, there is something to do about it. Sometimes, the only winning move is not to play.”

Burry reportedly opened 50,000 put options worth $9.2 million, with a strike price of $50 expiring in 2027. This represents a very large bearish bet.

In an interview with CNBC, Bill Gates said when asked about AI, “AI is only a bubble in the sense that not all of these valuations will rise. Some will fall… A reasonable percentage of those companies won’t be worth that much.”

“Sarah Friar, the CFO of OpenAI, said the company wants a federal guarantee to make it easier to finance massive investments in AI chips for data centers. Friar made the remarks at WSJ’s Tech Live event in California.”

— The Wall Street Journal

Is there enough demand for AI to justify these valuations?

User growth alone does not determine financial sustainability. The key question is unit economics — how much revenue is generated per user relative to the cost of serving that user. Unlike traditional software, AI systems incur ongoing costs for compute, storage, and electricity with every interaction. If revenue per user does not rise faster than these marginal costs fall, scaling usage may worsen, rather than improve, profitability.

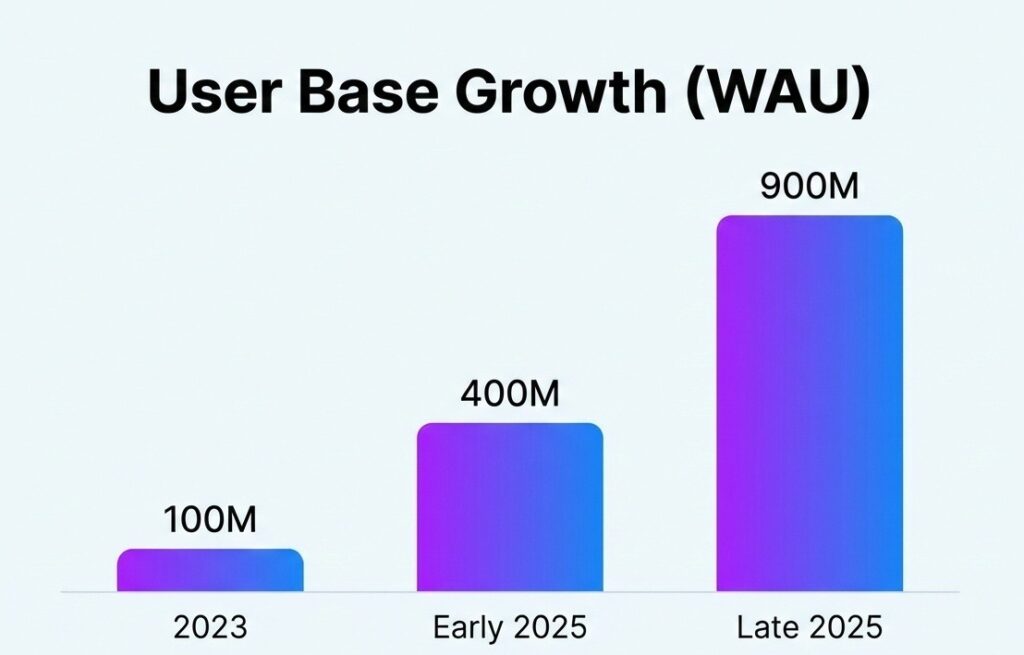

The data shows a clear and rapid verticality in user adoption. Between August and October 2024, the growth rate more than doubled compared to the previous nine months. While it doesn’t account for the costs of serving these users, it provides clear evidence that the user-side demand for the technology remained strong and rising through late 2024.

However, because these figures are self-reported by OpenAI, they carry the standard caveats of platform-internal metrics. Specifically, the introduction of ‘logged-out’ access in early 2024—allowing users to interact with ChatGPT without an account—introduces the possibility of inflated unique user counts. A single individual accessing the tool from different browsers, devices, or VPN locations could be registered as multiple ‘anonymous’ weekly active users. This distinction is critical: the graph may represent 250 million unique connections or sessions rather than 250 million unique human beings. Whether this discrepancy represents a minor margin of error or a significant overestimation remains an open question for market analysts.

High engagement metrics demonstrate interest in AI tools, but engagement does not automatically translate into monetizable demand. The critical test is whether users — particularly enterprises — are willing to pay prices sufficient to offset the growing cost of infrastructure.

OpenAI reportedly has around 10 million paid users, which signals monetizable demand but does not, by itself, justify current valuations. While paid subscribers demonstrate willingness to pay, the number remains small relative to the scale of infrastructure investment. The key uncertainties are ARPU (average revenue per user), the share of higher-margin enterprise and API revenue, and whether these revenues can scale fast enough to cover ongoing compute, storage, and energy costs.

Conclusion

The available data shows several warning signs consistent with an AI bubble, including valuation multiples far above fundamentals, capital expenditures that outpace revenue, and uncertainty over whether paying demand can scale to cover infrastructure costs. At the same time, it is impossible to say with certainty whether this will result in a classic bubble outcome, as some transformative technologies have historically required heavy upfront investment. The widening gap between capex and revenue, combined with limited visibility into sustainable unit economics, places AI in a speculative phase that could resolve either as a bubble or as a costly but necessary investment cycle.